|

Executive Summary | Portfolio | Guru Analysis | Watch List |

|

Economy & Markets Stocks closed out 2019 on a high note. The Dow Jones Industrial Average gained 22.3% for the year, while the S&P 500 was up 28.9%, its best year since 2013. The technology-heavy Nasdaq also rose the most in six years, ending up 35.2%. All three indexes hit record highs in late December. As in the last few years, technology giants drove a big portion of the gains. Amazon, Alphabet, Facebook, Amazon and Microsoft lifted the indexes as investors continued to pile into the stocks. Low interest rates may be partly responsible. After raising rates four times in 2018, the Federal Reserve slashed rates three times in 2019, partially easing investor fears of a recession or economic slowdown. That sets up 2020 to be a year of relative stability, with lower economic risks and low inflation. The Fed is expected to hold steady this year, and lower borrowing costs could entice consumers to make big long-term investments like buying a house. Inflation is running below the Fed's 2% target, giving the central bank plenty of incentive to keep rates low. Positive news on the U.S. trade war with China could also be lifting stocks. The battle has been going on since early 2018 with each side slapping tariffs on hundreds of billions of dollars of each other's imports. President Trump has accused China of unfair trade practices and theft of technology and China has retaliated. But negotiators indicated some progress in late December, saying there is a so-called phase one deal that could be reached by the end of January that would reduce some U.S. tariffs in exchange for an agreement by China to buy more American agricultural products and provide protections for American technology. The U.S. also put on hold some tariffs that would have hit Chinese smartphones, toys and clothing before the holidays, and China cut some tariffs on U.S. goods. The Trump administration suggested last month that the phase one deal could be signed as early as mid-January. Of course, that's not the end to trade woes. The Trump administration has battles open on multiple fronts. While it moved to sign a new agreement between the U.S., Mexico and Canada, the administration is also looking at tariffs on a variety of European goods such as French wine and cheese and Spanish olive oil, among others. A strong job market and resilient consumers are also boosting stocks. Last month, the Commerce Department said economic output rose 2.1% in the last quarter of the year, about the same as the third quarter, which economists viewed as positive. A strong labor market convinced the Fed to keep interest rates unchanged at their December meeting. According to the latest figures, unemployment was 3.5% in December, sitting near a 50-year low. Disposable income rose and consumer spending also rose, a good sign for the economy. More than two-thirds of output is consumer spending. The year's top stock sectors include, not surprisingly, technology followed by consumer discretionary and industrials. The top performing stock of the year was Advanced Micro Devices, up 148%. Lam Research (up 119%), KLA Corp. (up 103.9%), Target Corp. (up 100.1%) and Chipotle Mexican Grill (up 93.8%) rounded out the top five stocks. The energy sector was the laggard in 2019, up nearly 6%. The year was also notable for a rotation back to value stocks, something that really picked up momentum in September. Some analysts expect this rotation to continue into 2020 because of interest rates and a turnaround in some economic indicators. Here were some of the economic data points released as 2020 kicked off: 1. Private payrolls rose 202,000 in December, more than estimated, according to ADP and Moody's Analytics. 2. Consumer confidence dipped in December, according to the Conference Board. The economy hasn't shown signs of weakening, but consumers aren't expecting growth to gain momentum in the early part of 2020. 3. U.S. third-quarter economic growth was unrevised at 2.1% but U.S. manufacturing production rose more than expected in November. 4. Homebuilder confidence jumped to the highest level in 20 years, according to the National Association of Home Builders/Wells Fargo Housing Market Index. Recommended Reading There may be an explanation why value stocks rallied in September when markets were calm. A new pattern developed over the last decade where value stock performance increased when the bond yield curve steepened, according to The Wall Street Journal. And the correlation has become more pronounced recently. It could reflect investor caution about companies that might struggle to access funding during a slowdown. And investors who are worried about slow growth could be gravitating to long-term bonds, forcing yields down. Read more here and see below for links to blog posts and articles you may have missed. Factor Focus: Morningstar found that volatility, size and momentum factors work the best out of seven strategies. Interestingly, style is near the bottom of the list. Value investing, which is perhaps the most academically supported factor, has been a disappointment according to the data. Read more Value Caution: BlackRock's Andrew Ang tells Institutional Investor that investors should be careful about going back to the value factor, even though some influential funds like AQR and Research Affiliates have argued it's time to buy inexpensive stocks. Read more New Economy: Oakmark Select fund manager Bill Nygren told Barron's he thinks Google and Netflix are value stocks. This shows his thinking on value as a strategy. In an asset-light economy, he is willing to look at companies that look expensive by traditional measures. Netflix is not cash flow positive, but is growing subscribers quickly and has pricing power. Read more Team Work: The team approach seems to work better for funds. Three-person steams outperform solo run funds by 58 percentage points, according to CNBC, citing a study by Michael Mauboussin at Blue Mountain Capital. Some 75% of actively managed funds are team managed, according to Morningstar. Read more Stock Tips: Veteran stock picker Peter Lynch recently shared some ideas on finding growth opportunities in Barron's. His best ideas were companies that had a good concept or were growth companies in non-growth industries, such as Stop & Shop and Dunkin Donuts. He also suggested it's better to get in on stocks that are just beginning their growth phase, and if you miss that window, look for turnarounds or special situations. Read more Job Change: Berkshire Hathaway's Todd Combs took on a new job this year, becoming the chief executive of the car insurer Geico, according to WSJ. It's a big shift for the 48-year-old money manager, who helps oversee about $14 billion of Berkshire's massive investment portfolio. Read more New Market: Rob Arnott told CNBC's Trading Nation that a major market shift is on the horizon that could be a spectacular opportunity for value investors. The chairman of Research Affiliates says a rotation to value could be critical if the economy shifts. Read more Narrative Economics: Robert Shiller talked about his new book, Narrative Economics, in an interview with Barron's. Among the highlights, he said today's high stock valuations are about optimism and that getting over the financial crisis a decade ago required investors to forget the fear. He also admits to being ambivalent about the degree to which workers will be replaced by computers. Read more Value Time: RAFI Indices published a paper that said it's time to increase allocations to value strategies. RAFI's strategy focuses on rebalancing out of popular stocks and into stocks whose price has fallen and become undervalued. Read more Tech Rules: Tech giants Apple, Alphabet, Microsoft, Amazon, and Facebook contributed 20% of the S&P 500's growth last year despite all the worries about the effects of trade wars and regulatory crackdowns. Investors continued to pile into tech stocks, which seem resilient in the face of economic growth concerns. But tech's performance is remarkable because giant companies rarely see such growth. Read more Old Timers: Some of the oldest U.S. mutual funds - dating back a century - are still performing well, according to Barron's. Central Securities, Adams Diversified Equity and General American Investors, which are all closed end funds, gained 30% last year, beating the S&P. Read more Dividend Calculating: Barron's walked through the difficulty of calculating dividend yields on mutual funds. It's a little more complex than stocks, where you just divide the annual dividend per share by the price. Investors who rely on fund or advisor disclosures need to be aware of how the numbers are calculated. Read more International Stocks: Owning stocks of companies in developed countries around the world offers little diversification benefit, according to an article in CFA Institute. International stocks stopped outperforming U.S. stocks about 20 years ago and have underperformed since, and the allocation to U.S. stocks has slowly drifted up. The evolution of the global economy means the relationship between international and U.S. stocks has also changed. Read more ETF Update: Defunct ETFs hit 1,000 last year, often thinly traded funds that have wider spreads. In a sense, the whole ETF market is more of a meritocracy than mutual funds. ETFs have to attract assets from cost-obsessed picky advisors and investors, according to Bloomberg. Read more Avoiding Recession: Advisor Perspectives recently ran an interview of Wharton School professor Jeremy Siegel. The market, he says, is trading at 19 times earnings, up from 17-18 times a year ago because of low interest rates. He also says he's more confident the U.S. will avoid a recession over the next two years. Read more Volatility Bets: Investors shouldn't always trust calm markets, according to The Wall Street Journal. Market calm can be the result of investors betting against volatility rather than from external factors like geopolitical calm. This can blow up when all those trades unwind at the same time, as it did in early 2018. Read more Falling Fees: Active managers have taken steps to stop the flow of investing money to passive funds, but some of what they've done has hurt rather than helped. Investors are paying half as much to own U.S. mutual funds now compared to the 1990s but it still hasn't helped. Read more Eyeing Fundamentals: Profits, governance and price should be at the forefront of investment decision-making, according to Nir Kaissar in a recent Bloomberg article. He writes about SoftBank's recent missteps as a cautionary tale. Read more Pearce Profile: Randy Pearce at the Grandeur Peak International Stalwarts fund was recently profiled in Barron's about how they find opportunities in the stock market. The firm has an analytics team that has generated a three-year annualized return of 12.2%, which beat most others and the benchmark. Read more Overweight Stocks?: Fidelity's third quarter retirement report last month said Baby Boomers, who were born between 1944 and 1964, are too heavily weighted in stocks. This is the generation entering retirement now, and it's been riding a 10-year bull market. Nearly 10% of this age group is entirely invested in stocks, a risky bet. Read more |

|

||||||||||||||||||||||||||||||||||||||||

|

The Fallen As we rebalance the Validea Hot List, 1 stocks leave our portfolio. These include: Criteo Sa (Adr) (CRTO). The Keepers 9 stocks remain in the portfolio. They are: Oshkosh Corp (OSK), United Rentals, Inc. (URI), Skechers Usa Inc (SKX), Foot Locker, Inc. (FL), Bruker Corporation (BRKR), Meta Financial Group Inc. (CASH), Nk Lukoil Pao (Adr) (LUKOY), Onemain Holdings Inc (OMF) and Pennymac Financial Services Inc (PFSI). The New Additions We are adding 1 stocks to the portfolio. These include: Monster Beverage Corp (MNST). Latest Changes

The Perils of Market Forecasting If it's the new year, that means it's time for analysts to publish their outlooks. That means there's a whole lot of predicting going on, but that is fraught with danger for investors. Analysts have to make a name for themselves somehow, and predicting stock movements and setting price targets for the indexes and individual stocks is one way they do that. Some make bold predictions that grab attention, while others try to walk the middle of the road. Whatever their angle, Validea's Jack Forehand shares some thoughts for how much investors should pay attention. It's that time of year again. The time of year where all the market experts make their 2020 predictions. You will see countless forecasts about what the economy will do in 2020. You will see many experts tell you what interest rates will do next year. And most of all, you will see a variety of predictions for where the S&P 500 is heading this year. The experts making these predictions will even do you the favor of giving you exact price targets so you know exactly what will happen. But there will be one major problem with almost all of these predictions: They will be wrong. I could try to explain why short-term forecasting is a waste of time, but I couldn't do it any better than this quote from Jim O'Shaughnessy, the founder of O'Shaughnessy Asset Management. Here is Jim's take on short-term forecasting. And so, from our perspective, trying to make a successful forecast, short-term forecast, is a virtual impossibility, because, in the short term, there's quite a bit of noise in the marketplace. And people mistake noise for signal, and they have a narrative about it, and it's very believable, but unfortunately, often wrong. So we don't make forecasts in terms of what the market's going to do over short periods of time because quite frankly, we don't know. And if others were honest, they would have to admit that they don't know, either. source: https://25iq.com/2018/07/21/lessons-from-jim-oshaughnessy/ Most forecasts are made out of self-interest. The goal is more to bring attention to the forecaster than to actually benefit investors. They also follow some common themes. So as we work our way through the height of the annual forecast season, I thought it might be a good time to point out some of the tricks of the trade. Here are some types of forecasts you should watch out for.

The Calendar Year Prediction Predicting what will happen over a one-year period in the market is very difficult. Doing it consistently is essentially impossible. Yet every year, many of the top strategies at Wall Street's most prestigious firms not only try to predict whether the market will go up or down, but they try to do it with complete accuracy by setting exact price targets. This exercise can be great for entertainment purposes, but it should have no impact on how you manage your portfolio. To show how difficult this is to do, here are the year-end targets from analysts at some major Wall Street firms coming into 2019. As of this writing, the S&P 500 is at 3221. None of them were close. That isn't because they aren't smart or they aren't skilled. It is because they were trying to predict something that is impossible to predict.

source: Barrons, 2019 Outlook: U.S. Stocks Could Rally About 10%

The Doom and Gloom The playbook for this one is simple. You start by predicting that the stock market is in for a major decline. You talk about things like excessive debt that will break the system or extreme overvaluations. You might even present a chart or two that you have hand picked to best support your case. Then you repeat the process every single year until the decline you have predicted eventually comes. After that, you let everyone know you saw it coming and that investors would be well served by heeding your warnings going forward. What you will ignore is the fact that the market likely went up substantially from the point of your initial prediction, and that investors who followed you lost much more money missing those gains than they saved by missing the decline. We have seen these types of predictions throughout this bull market. Some have been making the bear case since 2009, while others jumped on at some point along the way. But the one thing they all have in common is they have been wrong. Making the negative case for stocks can generate great headlines. Anyone who does it will also ultimately be proven right at some point. But for these types of predictions to have any value, they need to not only get the timing of the decline right, but also need to come close to timing the bottom. History tells us that almost none of the market pundits who try to do this can do it successfully. And those who can are probably trading their own and their client's money and not telling everyone about it on Twitter.

The Crazy Prediction If I want to get attention for my market call, I am not going to predict a 10% increase in the market this year. I need to predict something much bolder. That way, if I am right, I will get lots of publicity, but if I am wrong, everyone will probably forget I said it in the first place. From the perspective of getting the most attention, this approach makes sense. But from the perspective of the investor who listens to the prediction, it can be the most damaging. A good example of this are those who predicted that Bitcoin was going to $50,000 or $100,000 in a very short time when it had made its run up to $20,000. Those predictions were very unlikely to ever come true, but they had huge upside for those who made them if they worked out. And when they didn't, most people just forgot about them.

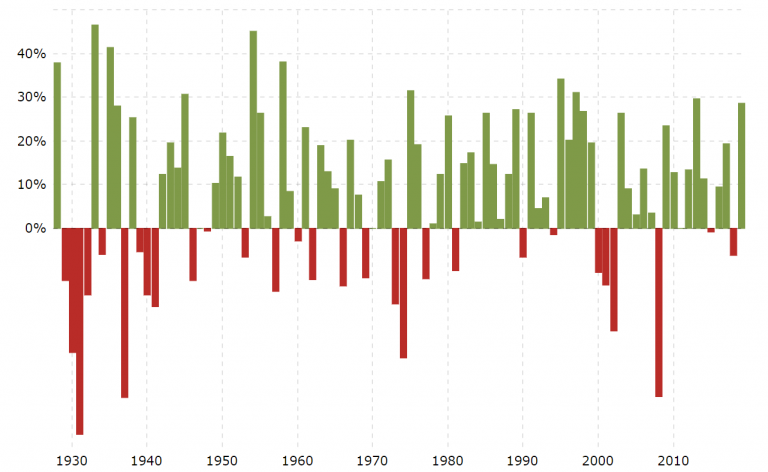

The "I Have No Idea So I Will Just Predict the Average" This is the exact opposite of the previous one and circles back around to those year-end Wall Street analyst forecasts I talked about before. If the market averages a 10 percent return per year and you want to limit your career risk from being wrong, the best approach is to just predict something close to that. That, however, doesn't consider the variability of returns. On average, the market returns about 10% per year over time, but the individual year returns are rarely close to that average. The chart below illustrates this concept by showing the annual returns of the S&P 500. Predicting a 10% return per year may be safe, but it is rarely correct.

source: https://www.macrotrends.net/2526/sp-500-historical-annual-returns

The Heads I Win, Tails I Also Win The best-case scenario for a forecast is setting it up in such a way that it can't be wrong. For example, I could predict that there is a 40% chance that we will have a bear market in 2020. By making a prediction like that, I have set myself up to claim victory no matter what happens. The odds of a bear market in any given year have been less than 40% historically. So if we get one, I can say that I called for above average odds of a bear market. But 40% is still less than an even bet. So if we don't, I can talk about how I predicted a less than 50% chance of a bear market. Either way, I win. Either way, I get to say I was right. The Dangers of Predicting the Unpredictable These are just a few examples of the type of market forecasts I have seen. The one thing they all have in common is that they should be looked at as entertainment and not as a reason to make any changes in your portfolio. So as you read this year's market forecasts, keep in mind that while they may be interesting, and may seem compelling when you read them, they will likely have limited value in telling you what is likely to happen in the future. New to the Hot List Monster Beverage Corp. (MNST) - This soft drink maker scores highly on the models tracking the style of Warren Buffett and Partha Mohanram. News on Hot List Stocks Russia's crude oil production could rise to more than 12 million barrels per day by 2035 if global demand continues to grow, according to a forecast by Lukoil. United Rentals should benefit from the positive construction market outlook as well as its strong technological and digital capabilities, according to Zacks Equity Research. |

|||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Guru Analysis

Watch ListThe top scoring stocks not currently in the Hot List portfolio.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Disclaimer |

|

The names of individuals (i.e., the 'gurus') appearing in this report are for identification purposes of

his methodology only, as derived by Validea.com from published sources, and are

not intended to suggest or imply any affiliation with or endorsement or even

agreement with this report personally by such gurus, or any knowledge or approval

by such persons of the content of this report. All trademarks, service marks and

tradenames appearing in this report are the property of their respective owners, and

are likewise used for identification purposes only.

Validea is not registered as a securities broker-dealer or investment advisor either with the U.S. Securities and Exchange Commission or with any state securities regulatory authority. Validea is not responsible for trades executed by users of this site based on the information included herein. The information presented on this website does not represent a recommendation to buy or sell stocks or any financial instrument nor is it intended as an endorsement of any security or investment. The information on this website is generic by nature and is not personalized to the specific situation of any individual. The user therefore bears complete responsibility for their own investment research and should seek the advice of a qualified investment professional prior to making any investment decisions. Performance results are based on model portfolios and do not reflect actual trading. Actual performance will vary based on a variety of factors, including market conditions and trading costs. Past performance is not necessarily indicative of future results. Individual stocks mentioned throughout this web site may be holdings in the managed portfolios of Validea Capital Management, a separate asset management firm founded by Validea.com founder John Reese. Validea Capital Management, which is a separate legal entity and an SEC registered investment advisory firm, uses, in part, the strategies on the web site to select stocks for its clients. |